Texas Rideshare Insurance What Minimum Coverage Really Means

You are parked at the airport lot, waiting for that next ping. The app is on. You are in “phase one” officially. Most drivers think the state minimum liability is all they need. Ten thousand dollars for property damage sounds like a real number. It is a number, but a dangerous one.

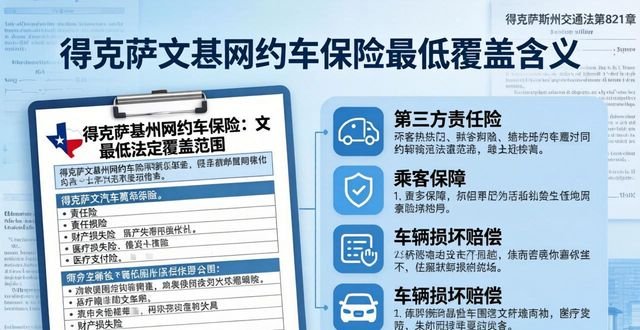

Let us start with a simple question. Why does Texas even set a minimum? The law wants every driver to have skin in the game. Thirty thousand for bodily injury per person, sixty thousand per accident, and twenty-five thousand for property damage. That is the famous 30/60/25. The government tells you this is enough to be legal. The government does not tell you this will protect you when a passenger spills coffee on a laptop while you are merging onto I-35.

Consider the ride hailed through an app. Your personal auto policy has a lovely clause buried on page fourteen. It says “livery or conveyance of passengers for a fee” is excluded. The moment you flip that app to “available,” your personal coverage winks out of existence like a ghost. You are driving naked. The rideshare company provides a contingent liability policy. That is another set of numbers. Fifty thousand dollars for bodily injury per person while you are waiting for a ride request. One million dollars once the passenger is in the car and the trip is active. But notice the gap. The gap is the time between trips. The gap is when you drive from the dropoff to the next hotspot. The gap is where the minimum coverage laughs at you.

A driver in Dallas learned this the hard way. He had the state minimum. He was between rides, heading to a busy intersection near the Galleria. A child ran into the street. He swerved and hit a parked Tesla. The damage was forty thousand dollars. His property damage limit was twenty-five. The difference came out of his savings, his tires, his ability to make next month’s car payment. The rideshare company’s contingent policy did not trigger because he had no passenger and no ride request accepted. He was in the gap. The minimum coverage sat there like a bad joke.

You might think the answer is simply to buy the rideshare endorsement from your personal insurer. Progressive,State Farm, Allstate, GEICO all sell it in Texas. The endorsement costs an extra twenty to forty dollars a month. For that price, it extends your collision and comprehensive coverage into phase one and phase two. But here is the twist. The endorsement does nothing to raise your liability limits. It only connects your personal liability to the rideshare gap. If you still carry 30/60/25 underneath, that is what you get. A fender bender with a Mercedes SUV will eat through twenty-five thousand dollars before the airbags finish deflating.

Why would anyone stick with the bare minimum? The answer is monthly cash flow. That driver earning twelve dollars an hour after expenses looks at his bank account and sees a choice. Pay the electric bill or pay for higher limits. The electric bill wins every time. The insurance industry knows this. They design the minimum to look like a helping hand. The hand holds a knife.

Let me show you the math that agents do not advertise. A minor accident with two vehicles and minor injuries averages forty thousand dollars in total costs in Texas today. The minimum property damage of twenty-five thousand leaves a fifteen thousand dollar gap. The bodily injury of thirty thousand per person covers about one day in a hospital intensive care unit. Two days if you are lucky. The passenger in the other car breaks a wrist. The bill arrives. The surgeon wants payment. Your minimum coverage says “I did my part.” The passenger’s health insurance sues you. The lawyer sends letters. The court orders garnishment. All because you saved fifteen dollars a month on your premium.

The rideshare company will not remind you of this during onboarding. Their training video talks about rating systems and cleaning vomit from back seats. It does not discuss umbrella policies or stacked limits. It does not mention that their one million dollar policy only activates when the trip is active. Between rides, you are a turtle without a shell. The minimum coverage is a paper umbrella in a hurricane.

You might ask why Texas does not raise the minimum. The lobbyists for insurance companies argue that affordable coverage is a social good. They say drivers need access to legal compliance. What they mean is that low limits keep premiums low, which keeps drivers on the road, which keeps their commercial policies profitable. The legislators nod and move on to zoning laws. The driver sits in his Honda Civic, unaware that his legal coverage is a trap door.

A better path exists. Ask your agent for a rideshare endorsement with liability limits of 100/300/100. The cost difference is eight to fifteen dollars more than the minimum endorsement. That extra money buys you protection against a ruined life. It buys you the ability to hit a doctor’s car without losing your home. It buys you sleep at night when the app sends you into a neighborhood of luxury SUVs. The minimum covers the law. The higher limits cover reality.

Remember that driver in the airport lot? He switched to fifty thousand property damage after the Tesla incident. He now tells every new driver the same thing. The state minimum is a suggestion, not a shield. You are one intersection away from owing more money than you will earn this year. The rideshare app will keep pinging. The passengers will keep rating. But the only number that matters is the one printed on your declarations page. Make it a number that does not haunt you.